States are being forced to show how they govern as federal pandemic relief runs out and structural deficits return. The budgets for Illinois and Maryland for fiscal year 2026 share a common blueprint: both are short billions of dollars, and both fund major social investments in education and healthcare, but their funding and spending plans are very different. Illinois is in Stabilization Mode, meaning it is focused on protecting credit gains and paying down old debts. Maryland is in “modernization mode,” which means changing tax policy to support long-term investments in education and social infrastructure. The question is not which model is better but which is more durable.

Illinois and Maryland may be separated by half a continent, but they are currently fighting the same fiscal war. As sovereign states, they act as the ultimate banks for their residents, yet both are reaching a breaking point. In the 2026 budget cycle, the “Blueprint” for state governance is being rewritten, pitting a desperate need for social investment against the hard reality of financial survival.

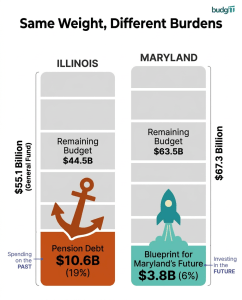

In the 2026 fiscal cycle, both states have had to navigate post-pandemic economic shifts, inflation, and evolving taxpayer expectations. While Illinois’s $55.1 billion General Fund budget primarily maintains the state and stabilizes pensions, Maryland’s $67.3 billion budget serves as a massive redistribution engine, funding healthcare and K-12 education to modernize the state’s social safety net. For years, federal pandemic relief has served as a safety net, enabling expanded spending, but now that the funding is gone, both states are facing massive budget gaps. However, the way they are choosing to fill these gaps shows two very different philosophies on government and growth.

Examining Illinois Fiscal Recovery Efforts

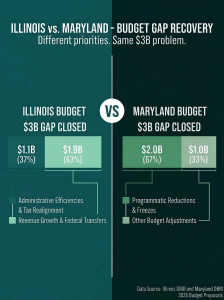

Illinois entered the 2026 budget cycle with the clear mission of protecting the credit upgrades of the last five years. Following decades of fiscal instability, the 2026 budget aimed to maintain the current course, even with a projected structural gap of nearly $3 billion, which has now stabilized through strategic adjustments and budget discipline.

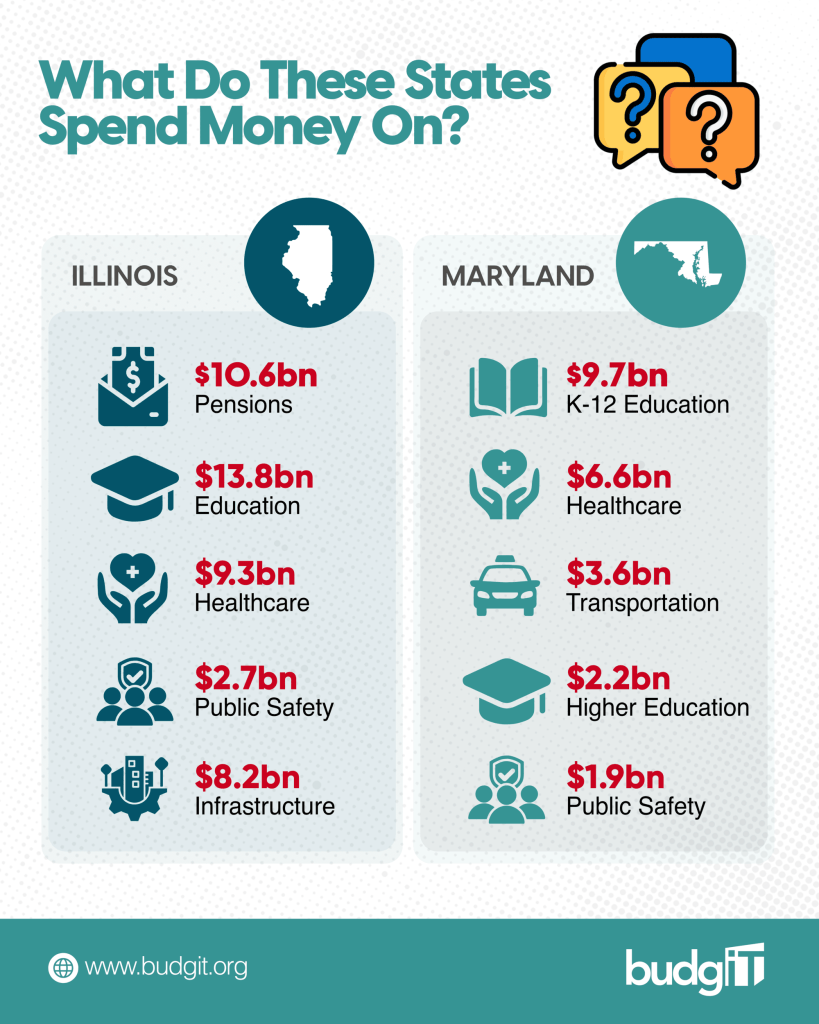

Instead of radical tax shifts, Governor J.B. Pritzker’s administration chose a “common-sense” stance on revenue enhancements and administrative efficiency. For this reason, the 2026 plan relied on a $1.1 billion mix of revenue adjustments, tax incentive programs, and the realignment of tax treatments for casino gaming. The primary focus for Illinois remains on balancing its hard costs. The state is fully funding its statutorily required $10.6 billion pension contribution, representing nearly 20% of its total general spending. However, by prioritizing these legacy debts and maintaining a $2.4 billion Rainy Day Fund, Illinois signals itself as a preservationist state focused on stabilizing the foundation so that its Smart Start Illinois investments in early childhood education can actually last.

Maryland is Restructuring for Long-Term Investment

While Illinois focuses on stabilizing its past, Maryland is doubling down on a vision for its future. As Maryland balances a $67.3 billion state budget and its own $3 billion shortfall, its approach to 2026 is less about raising funds and more about structurally changing who pays into the system. Governor Wes Moore’s administration is implementing a tax reform designed to reduce the tax burden on the middle class while asking more of the state’s highest earners. Under the 2026 plan, nearly two-thirds of Marylanders will receive a tax cut funded by creating new tax brackets for individuals who earn over $500,000 and $1 million. Additionally, Maryland is also exploring new industries by increasing taxes on sports wagering, table games, and cannabis.

Where Illinois is focused on securing its credit rating and debt obligations, Maryland is focused on securing its long-term investments. The 2026 Maryland budget allocates $3.8 billion to the “Blueprint for Maryland’s Future,” the landmark plan to reform Maryland’s education system. To ensure the smooth operation and transition of this plan, Governor Moore proposed a $2 billion cut to underperforming programs and a temporary funding freeze on some community school programs deemed ineffective. The aim of these cuts is to ensure that every child in the state has access to high-quality schooling.

Comparing Both States’ Fiscal Philosophies: Illinois vs.Philosophies

There are three ways to understand the difference between Illinois and Maryland:

- Debt versus Future Obligations

Illinois’s top priority is paying down old debts, especially pensions, to restore long-term stability. Even though Maryland is dealing with short-term deficits, it prioritizes long-term social infrastructure, especially education reform.

- Revenue Strategy

Illinois makes small, targeted changes to its revenue to avoid giving the impression that things are unstable. Maryland is making progressive changes to its tax system, raising the tax burden on higher earners while protecting middle-income households.

- Risk Profile

The main risk for Illinois is that its structures are too rigid. High pension costs make it challenging to be flexible with money. Maryland’s biggest risk is that its income will change. Relying too much on high earners makes you more vulnerable during downturns.

Both states want to be financially responsible. They just have different definitions. Illinois says that being responsible means fixing the past before moving on to the future. Maryland says that being responsible means changing the future while keeping things in balance.

The contrast between the two states lies in their methods of survival. Illinois is in “Stabilization Mode,” carefully managing its recovery from near-junk credit status by prioritizing pension payments and building rainy-day reserves. This focus seeks to demonstrate that Illinois is a reliable and steady place for businesses and residents alike. Maryland, on the other hand, is in a statewide “Modernization Mode,” which is why it decided to shift tax burdens to the wealthy so as to make provisions and safeguard its long-term investments in education and healthcare.

Despite the varying focus of Illinois and Maryland, both budgets share a common goal. This goal is to prove that the government can be fiscally responsible and socially just, even when the federal safety net has run out. Although both states are not without their shortcomings and setbacks, there have, however, been progressive policies that continue to advance the budget focus. While we are still in the early part of the year, we can only watch and see how far our governments are willing to keep the promises they have made to us, and whether they can advance the state of affairs in their respective jurisdictions.

Broader Structural Context

Federal funding changes affect both states differently. Medicaid matching rates, infrastructure funding, and education grants remain important sources of income. Any cuts made by the federal government would significantly impact both budgets.

Economic composition also matters. Illinois’ economy is anchored by Chicago’s financial and logistics, and manufacturing sectors. Maryland’s economy is closely linked to federal employment and contracting activity because of its proximity to Washington, D.C. These structural differences affect its revenue stability and risk exposure.

Accountability Watch Points for FY2026

The most important things for observers, analysts, and residents to keep an eye on are:

Illinois

- Trends in pension funding ratios

- The growth or loss of the Rainy Day Fund

- Changes in the outlook for credit ratings

- How revenue performance compares to projections

Maryland

- How well does high-income tax revenue work?

- Standards for putting the blueprint into action

- Predictions of structural deficits in the future

- How much money gaming and cannabis make compared to what was expected

Budget success will not be measured solely by FY2026 balance sheets, but by durability over the next three to five years.

Final Thoughts

Illinois and Maryland are confronting similar fiscal realities, but they are taking different paths to solve them. Illinois is attempting to solidify its recovery by maintaining discipline and signaling stability to capital markets. By restructuring taxes and making consistent investments in education, Maryland is modernizing its social contract.

There is a risk with both models. Both models show a clear plan. The real test will be resilience. Can Illinois maintain stabilization without sacrificing growth and innovation? Can Maryland modernize without destabilizing its revenue base? As federal support wanes and economic uncertainty persists, these two approaches will offer a revealing case study in how states balance fiscal credibility with social ambition.

Abiola Afolabi, International Growth Director at BudgIT, and Rebecca Nzerem, Research and Communications Officer at BudgIT, write from Chicago, IL.