Illinois and Maryland entered the post-pandemic era with two very different fiscal philosophies. One focused on stabilizing its finances and repairing decades of debt. The other doubled down on long-term investment and economic modernization. But FY2027 may be the first real stress test for both strategies. This is the second part of our ongoing series on state fiscal strategy. Read Part 1: Budgeting for the Future: Illinois’ Stabilization Strategy vs. Maryland’s Modernization Agenda. This piece examines what has changed, what has held, and what the FY2027 budgets reveal about each state’s evolving fiscal identity.

When we last examined these two states, both were navigating the end of the federal pandemic relief and maximizing different approaches. Illinois, on the one hand, was quietly paying down debt and rebuilding its reserves, while Maryland was overhauling its tax code and accelerating investments in education. With the new fiscal year fast approaching, both states have had to adjust their plans, and Maryland has had to change direction.

FY2027 shows that both Illinois and Maryland have shifted away from primarily focusing on post-pandemic recovery. They are now managing federal retrenchment. Illinois estimates its funds owed or withheld by the federal government to be at $8.4 billion, and Maryland has absorbed the loss of approximately 25,000 federal jobs. Neither state’s plans anticipated these pressures in 2026, and FY 2027 is, in many ways, the first budget under the new reality of federal cuts. The core comparison of different strategies still stands, but the FY2027 budgets reveal important nuances in how each state is evolving its plans under federal pressure.

Examining Fiscal Recovery Efforts

The budgets for Illinois and Maryland for fiscal year 2027 share a common blueprint: both are short billions of dollars, and both fund major social investments in education and healthcare, but their funding and spending plans are very different. Illinois is still in a Stabilization Mode, which means it focuses on protecting credit gains and paying down old debts. Maryland has pivoted in FY 2027 toward a stricter fiscal outlook, closing a $1.5 billion deficit without raising new taxes or fees while protecting its signature education investments. The question now is not which model is better but which is more durable.

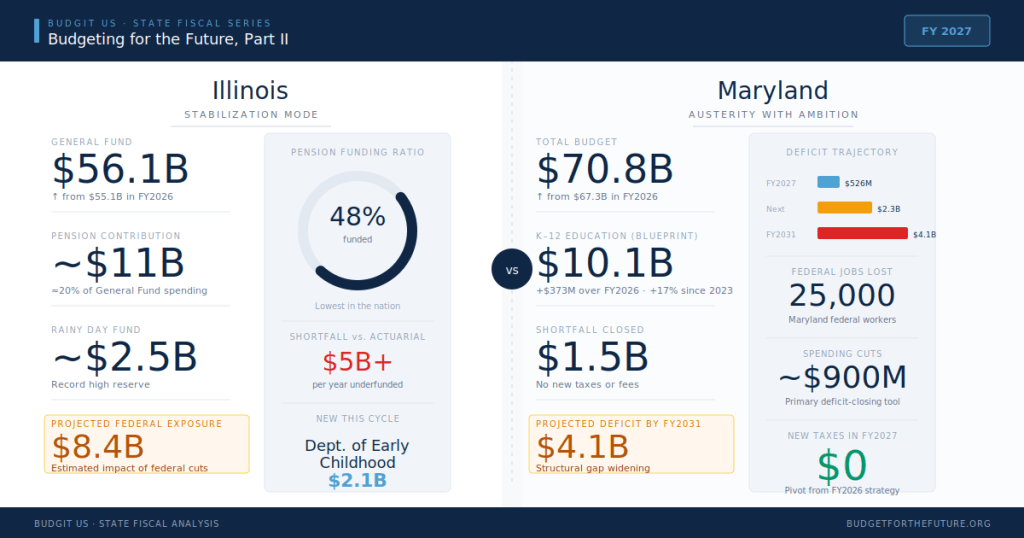

While Illinois is using its $56 billion budget to prioritize stability and debt management, Maryland is pivoting to a historically lean $70.8 billion budget featuring its smallest spending increase in decades.

Illinois

Governor Pritzker’s $56 billion General Fund budget, which is higher than FY2026, continues the state’s streak of balanced budgets while keeping stabilization at its core. The biggest headline is its pension contribution, which has reached a staggering $11 billion, the highest in the state’s history and representing nearly 20% of Illinois’ total General Fund spending. The Rainy Day Fund has grown to nearly $2.5 billion, another historical figure far from the $60,000 it held when COVID hit. Essentially, these are the metrics Illinois pointed to in FY2026 as proof of its recovery, and they remain the state’s strongest argument for continued credit improvement.

However, it is important to note that the margin of optimism has narrowed since a year ago. The FY2027 plan relies on roughly $589 million in new revenue-generating initiatives, including a $269 million cap on corporate net operating loss deductions and a $200 million social media platform fee, alongside $1 billion in updated revenue assumptions. The primary focus for Illinois remains on balancing its hard costs. But critics note that banking on updated projections to close a structural gap is a recurring Illinois habit that leaves the budget exposed if collections underperform.

Furthermore, Illinois’ pension situation deserves a more candid framing than the FY2026 analysis provided, because while Illinois is meeting its statutory obligation, that obligation remains more than $5 billion short of what actuaries recommend. The state’s pension funding ratio is just 47.7%, the lowest in the nation, while its total unfunded liabilities are around $143 billion. However, one meaningful structural change from FY2026 is the creation of the new Department of Early Childhood, a roughly $3 billion consolidation of previous scattered early childhood programs and investments. This is the kind of modernization that Illinois has struggled to execute, so the success or failure of this initiative will be worth tracking.

Maryland is Restructuring for Long-Term Investment

While Illinois focuses on stabilizing its past, Maryland is managing a notable strategic pivot. Having balanced a $3.3 billion structural deficit in FY 2026 through a combination of cuts, fund transfers, and $1.6 billion in new taxes on high earners, Maryland’s FY2027 approach is decidedly more rigorous. Governor Wes Moore’s $70.8 billion budget proposal includes no new taxes or fees, closes a $1.5 billion shortfall primarily through nearly $900 million in targeted spending cuts, and focuses on government efficiency. Moore attributed the deficit to the Trump administration’s reductions in the federal workforce.

Where Illinois focuses on securing its credit rating and debt obligations, Maryland focuses on securing its long-term investments. The 2027 Maryland budget allocates $10.2 billion to K-12 education, which is a $373.8 million increase over FY 2026 and a nearly 17% rise since the start of the Moore-Miller administration. The state’s 10-year Blueprint for Maryland’s future, designed to increase annual education funding by about $3.8 billion by 2032, continues to phase in. However, analysts warn that the Blueprint fund faces a growing structural shortfall of its own, with ongoing revenues insufficient to cover increasing program costs beyond 2026. The aim of these cuts is to ensure that every child in the state has access to high-quality schooling. However, many speculate that Maryland’s current FY 2027 “no new taxes” posture may be a temporary political reprieve rather than a structural fix.

What Has Changed and What Hasn’t

In Part I, we framed the contrast between Illinois and Maryland around three axes: debt vs. future obligations, revenue strategy, and risk profile. Here’s how each dimension looks for FY2027:

- Debt versus Future Obligations: Illinois’s position is largely unchanged, as pension debt still dominates the balance sheet, and the state’s primary obligation remains paying it down incrementally. The $11 billion statutory contribution in FY2027 is a continuation of routine, not a new commitment. On the other hand, Maryland’s position has become more complex. Illinois is seeking long-term credibility through fiscal restraint. Maryland is attempting to buy long-term competitiveness through public investment.

- Revenue Strategy: There are significant changes to revenue strategies in both states. In FY2026, Maryland rewrote its tax code, while Illinois made incremental adjustments. In FY2027, those roles have reversed as we see Illinois reaching for new revenue levers (corporate tax cap, Social media tax), while Maryland is holding the line on taxes. Neither approach is risk-free and reveals structural vulnerabilities and deferrals rather than long-term solutions.

- Risk Profile: Both states have seen their risk profiles shift. Illinois’s rigid structures, with high pension costs limiting fiscal flexibility, remain unchanged but are now compounded by $8.4 billion in projected federal exposure. While Maryland’s revenue concentration has shifted from reliance on high earners to reliance on federal employment.

The Bigger Picture

One of the most important takeaways from comparing these two FY2027 budgets is what they reveal about the limits of state fiscal strategy when faced with federal policy hurdles. Both governors have framed their budget challenges in terms of federal actions rather than state mismanagement, and in both cases, they have a point.

Prior to the federal fund cuts, the underlying assumption was that states were the primary agents of their own fiscal health, with federal funding as a stable backdrop. However, the reality of FY2027 paints a different story. With Medicaid matching rates, SNAP funding, federal workforce levels, and infrastructure grants all competing for attention, Illinois and Maryland, with their significant populations, are budgeting in conditions that require intense flexibility and rigorous line-item discipline. So the question now is whether both states can find long-term solutions to the current federal cuts, and whether their new approaches will hold till the end of FY2027.

Accountability Watch Points

Here is what to monitor as FY2027 unfolds:

Illinois

- Whether $1 billion in revised revenue assumptions materializes or triggers mid-year pressure

- Pension funding ratio trends and any movement toward actuarially recommended contributions

- Rainy Day Fund stability near the $2.5 billion mark, as federal funding uncertainty plays out

- Implementation quality of the new Department of Early Childhood

- Credit rating outlook, particularly how agencies weigh federal exposure vs. continued fiscal discipline.

Maryland

- Whether the “no new taxes” stance holds as the structural deficit widens in the next term

- The gap between the Blueprint for Maryland’s Future program costs and dedicated revenues is growing

- Income tax and consumer spending revenue trends are tied to federal job losses in the state

- Long-term structural deficit trajectory through FY2031

- Whether the FY2026 high-earner tax bracket changes generate the sustained revenue assumed in multi-year projections

Budget success will not be measured solely by FY2027 balance sheets but by durability over the next three to five years.

Final Thoughts

In our earlier analysis, we asked whether Illinois’ stabilization model or Maryland’s modernization model would prove more durable. FY2027 does not settle that question, but it meaningfully reframes it. Illinois has shown that stabilization can be sustained even under external pressure, but it also reveals the structural time bomb that no amount of Rainy Day Fund discipline alone can defuse. Maryland has also shown its grit in protecting signature investments, but its longer-term deficit trajectory is concerning and poses a significant risk to its modernization strategy.

The most important question for FY2028 and beyond is whether either state can sustain its chosen path if federal support continues to erode. That is the story we will have to keep watching unfold.

Rebecca Nzerem, Research and Communications Officer, writes from Chicago, IL.